Net worth is the one number that tells you whether all your financial decisions are actually moving you forward. This free Google Sheets template tracks it automatically across your checking, investment, credit, and loan accounts. Add balances manually each month, or connect Finta to keep them current daily. No complicated setup, no spreadsheet wizardry.

What is net worth (and why should you track it)?

The simple definition

Net worth = what you own minus what you owe. Add up your bank accounts, investments, and property (your assets). Subtract your credit cards, loans, and mortgage (your liabilities). The number you're left with is your net worth, the clearest snapshot of your financial health.

Most people check their bank balance daily but calculate their net worth... never? Once a year? That's like focusing on the trees while missing the forest. This template helps you track net worth regularly so you can see the full picture, not just this week's spending.

What you get

- A dashboard that actually makes sense

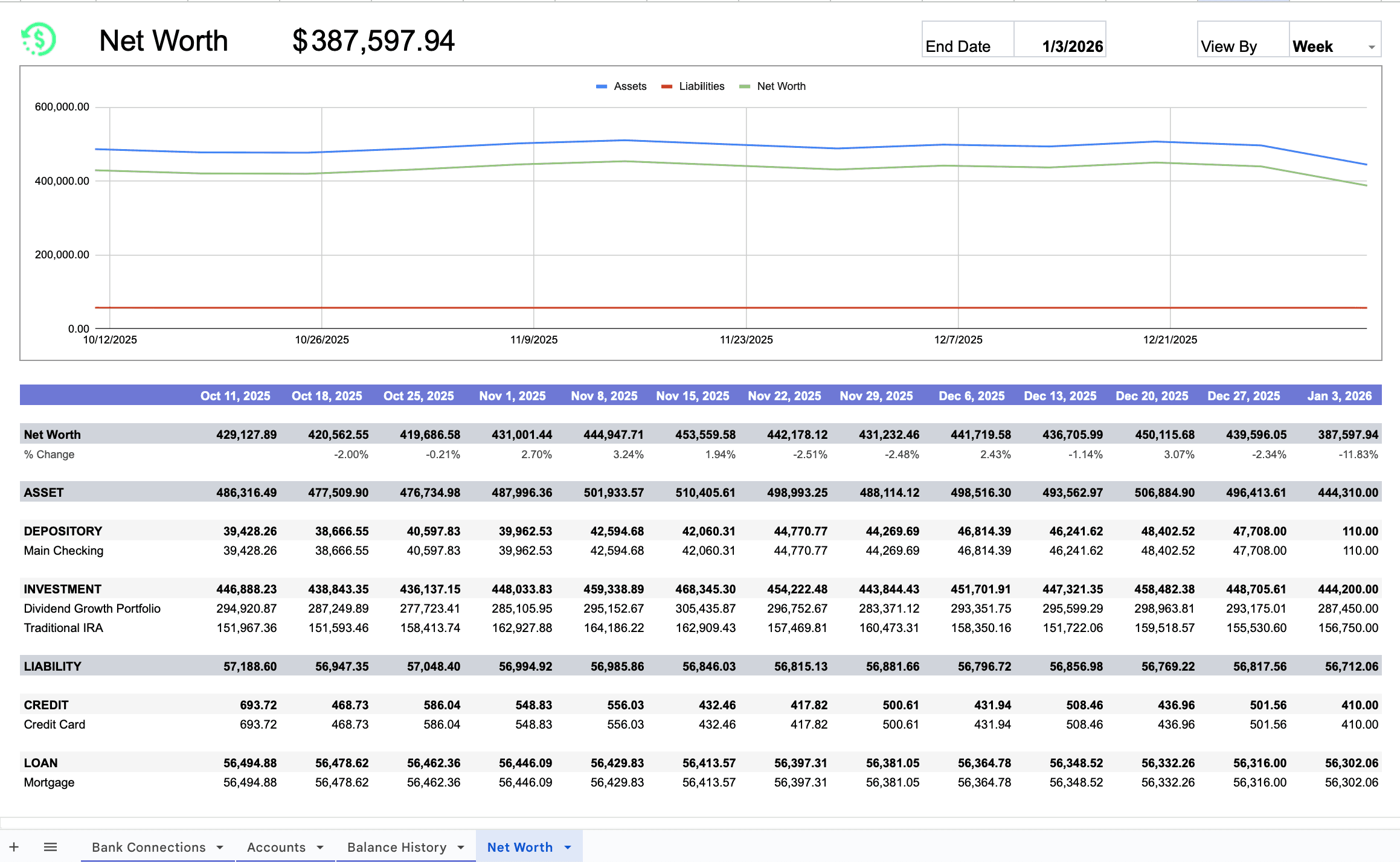

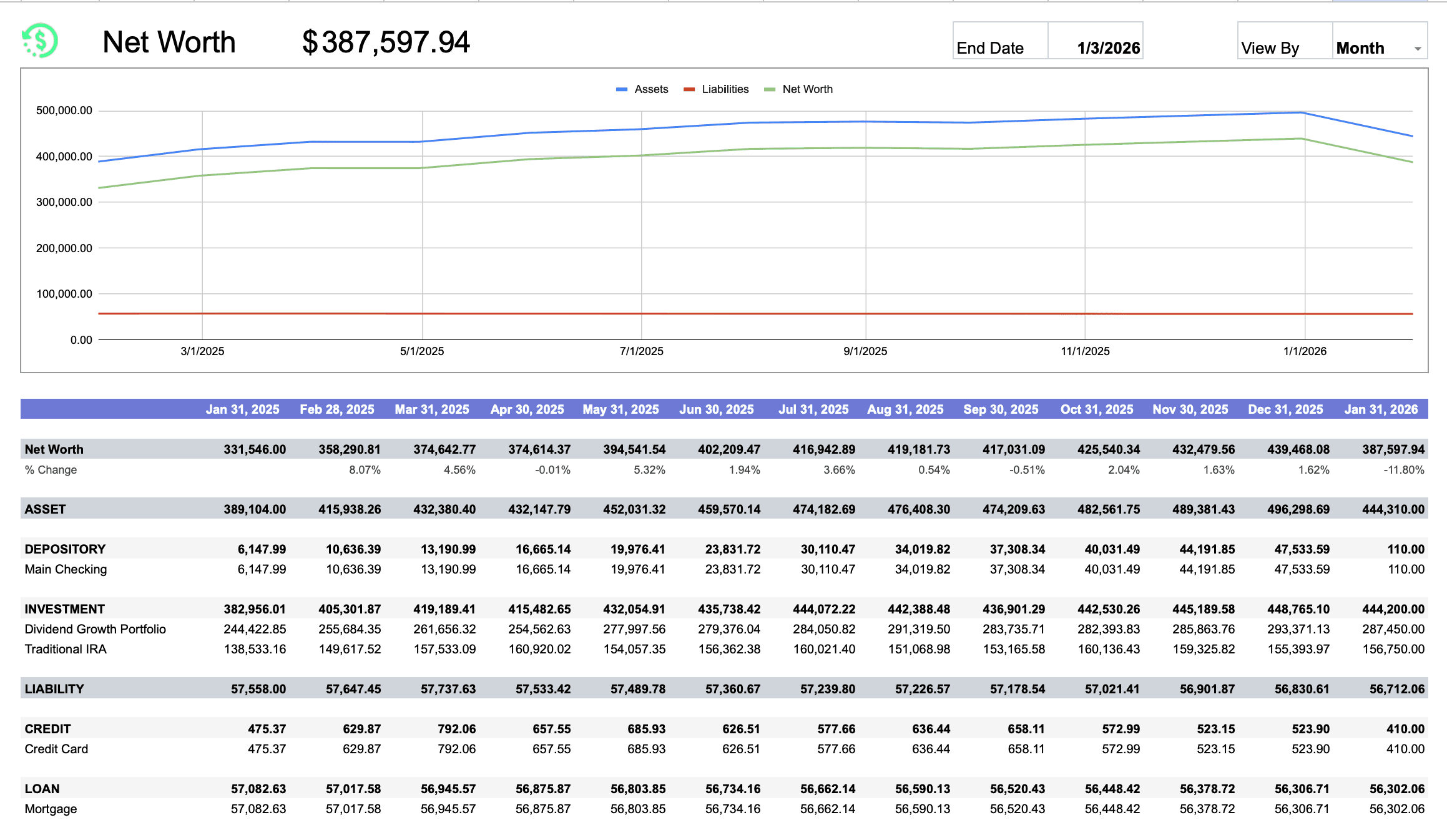

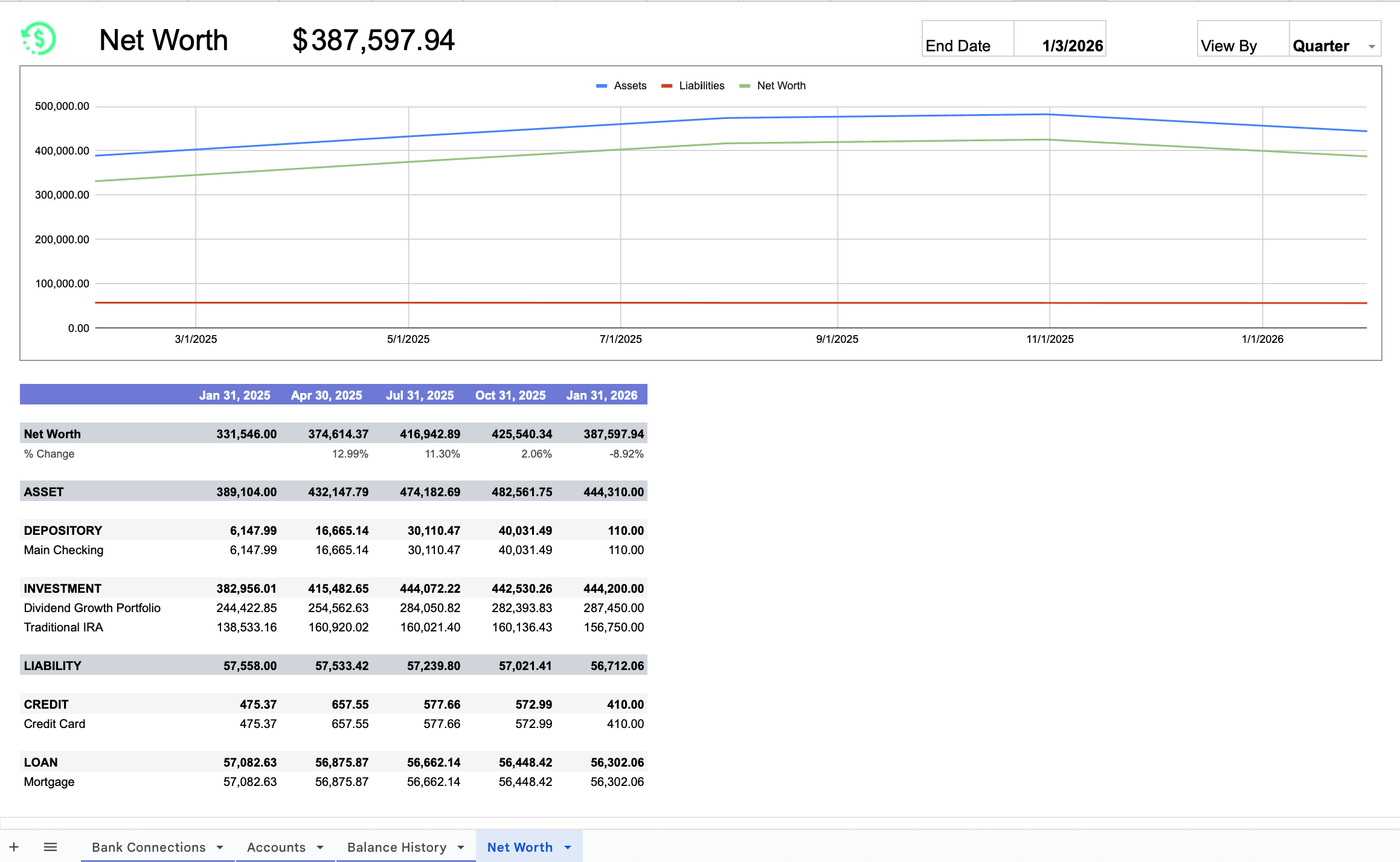

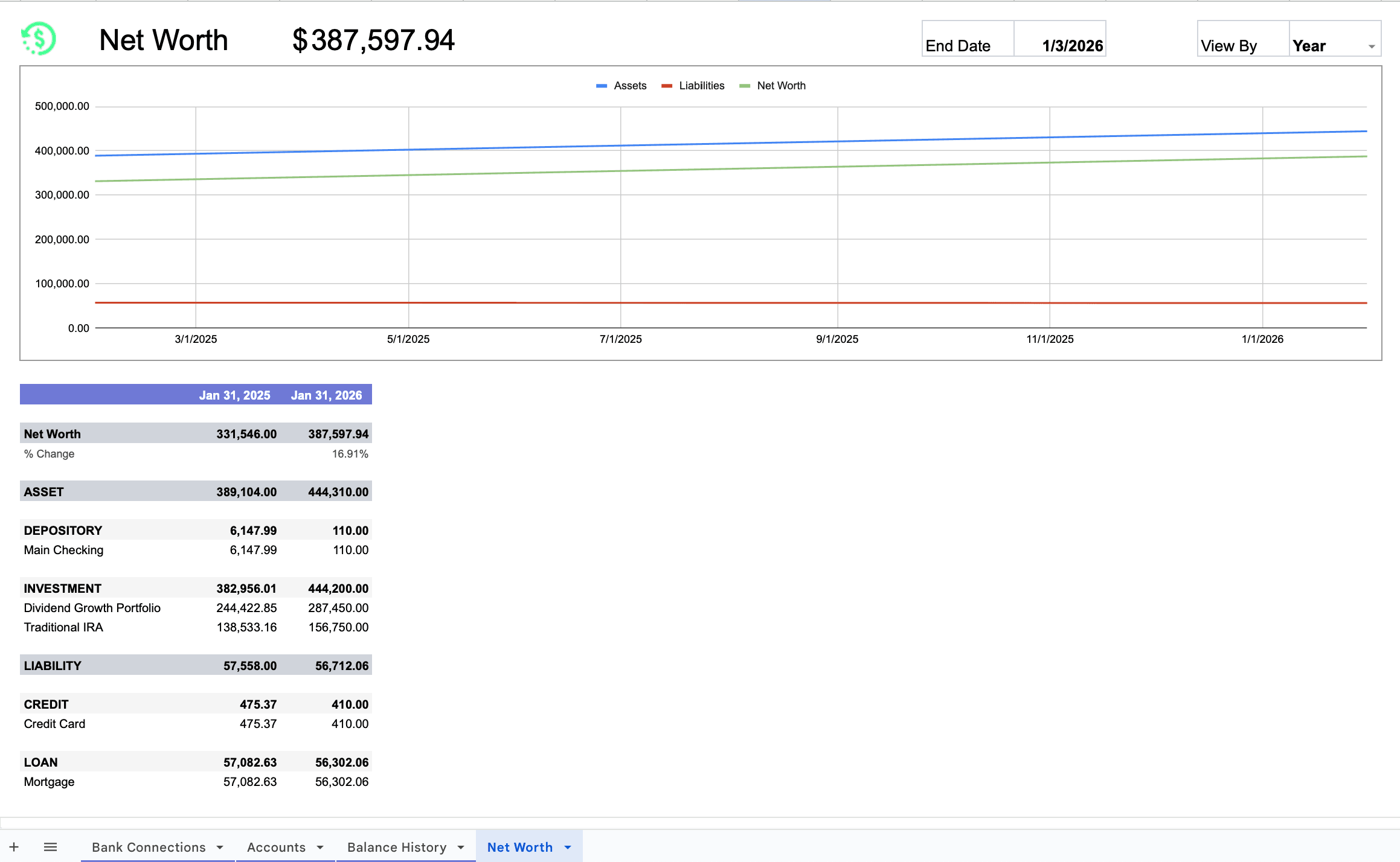

Open it up and immediately see your current net worth, how it's changed since last month, and what's driving the change. No hunting through tabs.

- Charts that show your progress

Built-in charts track your assets, liabilities, and net worth over time. Pick weekly, monthly, quarterly, or yearly and see how far you've come.

- Automatic calculations

Enter your balances and let the spreadsheet do the math. It sorts assets vs. liabilities, calculates totals, and figures out your growth rate.

- A place for every account

Bank accounts, 401(k), credit cards, mortgage, brokerage. Organize by type and see where your wealth is concentrated.

- Historical tracking built in

The balance history sheet stores snapshots over time so you can track trends and celebrate milestones. Looking back is surprisingly motivating.

- Works with Finta

Skip the manual updates. Connect your accounts to Finta and your balances refresh automatically every day.

How to get started

List your financial institutions

Start by adding the banks, brokerages, and lenders where you have accounts. Think of it as building your financial rolodex.

Add your accounts

For each institution, list the specific accounts: checking, savings, retirement on the asset side; credit cards, loans, and mortgages on the liability side.

Enter your current balances

Pop in today's numbers. The template figures out the rest, categorizing accounts and calculating your net worth automatically.

Update regularly

For manual tracking, once a month works great. Add new balance snapshots to the history sheet and watch your trend line develop.

Check your dashboard

Come back anytime to see where you stand. The dashboard updates automatically as you add data.

Want it to update itself? That's where Finta comes in

Manual tracking works, but life gets busy and spreadsheets get forgotten. Finta connects directly to Google Sheets and writes your balances in for you. Every day, automatically. Your balances stay current. No more logging into five different apps to copy numbers over. Finta syncs your accounts daily, so your net worth tracker always reflects reality. Your history builds itself. Every balance change gets recorded automatically. Come back in six months and see exactly how your wealth grew without having to remember to update anything. Your charts stay fresh. As new data flows in, your wealth trend charts update in real time. For the full setup walkthrough, see How to Sync Bank Accounts to Google Sheets.Accounts you can connect

If it has a balance in a U.S. bank, brokerage, or fintech, Finta probably supports it. The institutions Finta users connect most often for net worth tracking:

- Brokerages and retirement: Charles Schwab, Robinhood, Fidelity, Vanguard

- Banks and credit cards: Chase, Bank of America, Capital One, plus 12,000+ more

- Business banking: Mercury, Brex, Relay

- Crypto: Coinbase, Gemini, Kraken

- Stripe balances for online businesses

Why bother tracking net worth?

- It cuts through the noise

Income, expenses, savings rate all matter. But net worth is the scoreboard. It tells you if everything else is working. For context, the Federal Reserve's 2022 Survey of Consumer Finances put U.S. median household net worth at roughly $192,700, with the typical 35-to-44-year-old household sitting near $135,600. Wherever you land, the direction of the line is what matters.

- It keeps you honest

Feeling like you're making progress? Net worth confirms it (or gently suggests you adjust course).

- It shows the impact of big decisions

Buying a car, paying off debt, maxing out your 401(k). Net worth tracking shows you exactly how these choices move the needle.

- It spots problems early

A stagnating or shrinking net worth is a signal. Better to see it in a chart than feel it in a crisis.

- It makes goal-setting real

Want to hit $100K? $500K? Financial independence? Track your net worth and you'll know exactly how close you are.

Who uses a net worth tracker?

People just getting started

Seeing a single number beats juggling mental math across a dozen accounts.

Debt payoff warriors

Watch your liabilities shrink and net worth climb as you knock out balances.

Retirement planners

Track progress toward your number, whatever that number is for you.

Couples managing money together

One shared view of household wealth keeps everyone on the same page.

FIRE pursuers

Financial independence doesn't happen by accident. Track your way there.

Business owners

Separate personal wealth from business finances with clear visibility into both.

High earners with complex finances

Multiple accounts, multiple institutions, one consolidated view.

Anyone who wants clarity

You don't need to be a finance nerd. You just need to want to know where you stand.

Inside the template

Net worth

This is home base. At a glance: current net worth, period-over-period change, and a breakdown of assets vs. liabilities. Use the dropdown to switch between weekly, monthly, quarterly, and yearly views.

Bank connections

A simple list of everywhere your money lives: banks, brokerages, credit unions, lenders. When using Finta, this populates automatically.

Accounts

Every account you own, organized by type:

- Depository: checking, savings, money market

- Investment: 401(k), IRA, brokerage, HSA

- Credit: credit cards, HELOCs

- Loan: mortgage, auto, student, personal

Balance history

Snapshots of your account balances over time. This is what powers your trend charts. Manual users update this periodically; Finta users get automatic daily entries.

How the math works

- Total assets = all positive balances added up

- Total liabilities = all debts added up

- Net worth = Assets minus Liabilities

- Growth % = change from last period to this one

Everything updates automatically as you add data.

Real ways people use this

- Building an emergency fund

Watching your net worth climb as your savings grow is satisfying in a way that checking your bank balance isn't.

- Crushing debt

Every payment shrinks your liabilities and grows your net worth. Same progress, but visualized in a way that feels like winning.

- Growing investments

Market returns, dividends, contributions all show up in your net worth. See how regular investing compounds over months and years.

- Making big purchase decisions

Thinking about a home down payment or new car? See exactly how it'll affect your net worth before you commit.

- Planning for retirement

Set a target number and track your progress toward it. Adjust your savings rate based on real data, not guesswork.

- Rebalancing your portfolio

When one asset class outgrows the others, you'll see it in the breakdown. Spot imbalances before they become problems.

Tips for getting the most out of this

What works

- Include everything. Even small accounts add up. The point is a complete picture, not a curated highlight reel.

- Pick a rhythm and stick to it. Monthly updates are enough for most people. First of the month, five minutes, done. The Bogleheads community wiki recommends quarterly at minimum for anyone tracking by hand.

- Focus on the trend, not the number. A single snapshot means less than the direction you're heading. Are you up or down compared to three months ago? That's what matters.

- Don't panic over dips. Markets go down sometimes. One bad month doesn't undo years of progress. Zoom out.

- Set a growth goal. 5–10% annual net worth growth is a solid baseline. A target makes the tracking feel purposeful.

- Don't forget illiquid assets. Home equity, vehicles, business ownership. If it has real value, it belongs in your net worth.

Ready to know exactly where you stand? Grab this free net worth tracker for Google Sheets and start seeing your complete financial picture. Your future self will thank you.